There are 4 decisions every ASRS member must make before they retire that can significantly impact your financial security. Most people make these decisions without fully understanding their long-term consequences, or they’re unaware of all their options.

Today I’m going to walk you through each decision and show you the math so you can make informed choices that align with your retirement goals. Since some of these elections become permanent once you retire, understanding them now will help you feel confident about your financial future.

Decision #1: Survivor Benefit Election

This is probably the biggest financial decision you’ll make regarding your pension, and it’s permanent.

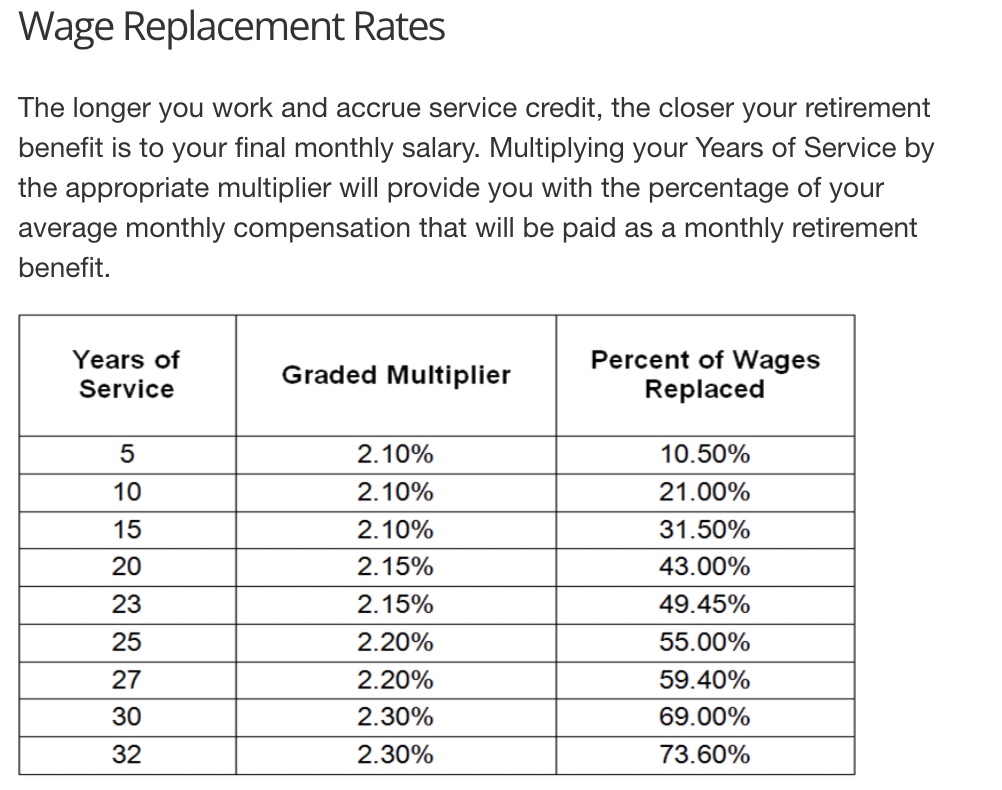

You have seven choices but let me cover two of the most popular ones. The first is a straight life annuity. You’ll get your pension payment for life, as long as you live. If your death occurs before all of your contributions plus interest have been paid, the remaining balance will be paid to your beneficiary. There is no ongoing benefit to a beneficiary in the event of the member’s death.

The next is the 100% joint and survivor option. This option provides a monthly benefit for life. If you die before your spouse, your spouse gets that same monthly pension for the rest of their life. Sounds great, right? But here’s the catch: you take a permanent reduction in your monthly benefit to allow your spouse to have the right to your pension if you die first.

Let’s say your pension would be $3,000 monthly as a straight life annuity. With the 100% joint and survivor option, you might only get $2,600 monthly. That’s a $400 difference every month. Now I’m just spitballing numbers here, and you absolutely should check this on your ASRS account to see the exact differences in your situation. I’m just trying to highlight the difference.

There’s also a middle ground with the “certain period” options – the 5-year, 10-year, and 15-year certain life annuities. These options guarantee that payments will continue for a specific period even if you die early. If you make it past the 5 or 10 or 15 year time period, then your pension will readjust to the straight life amount. And when you die after that, the pension stops entirely.

There is no “right” answer as it depends on your health, your spouse’s age and health, and your other income sources.

Decision #2: Retirement timing

This is obviously an extremely important decision, which you will live with the rest of your life and the life of your pension.

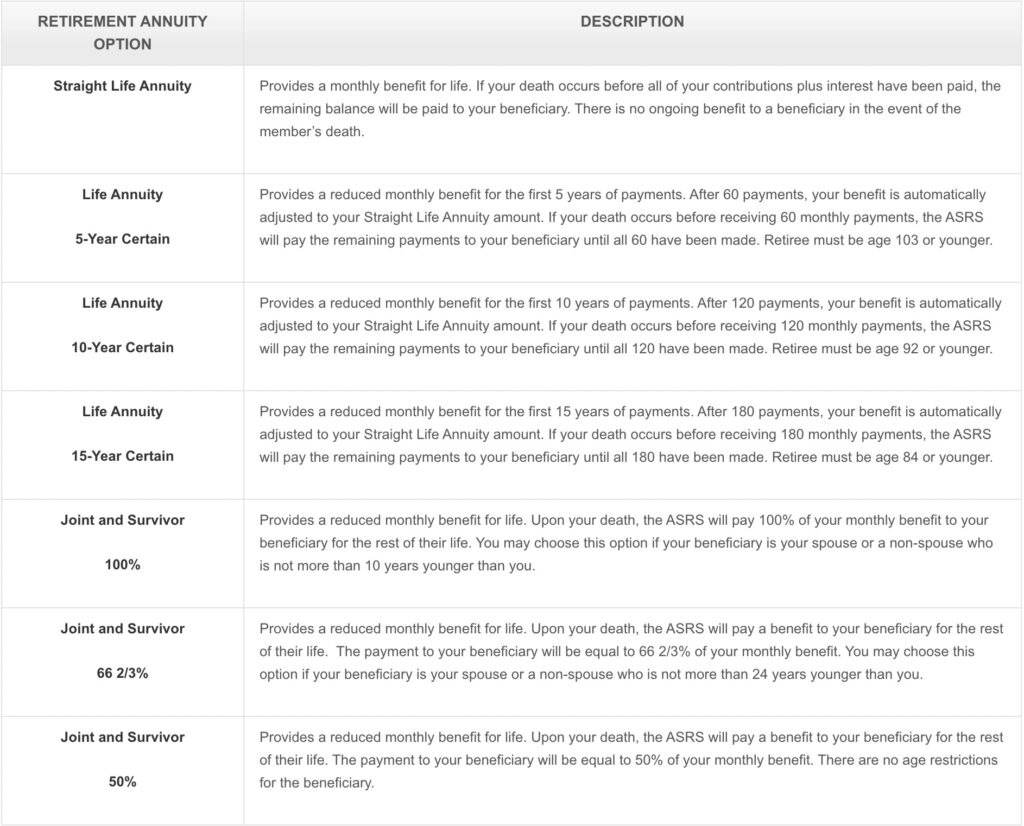

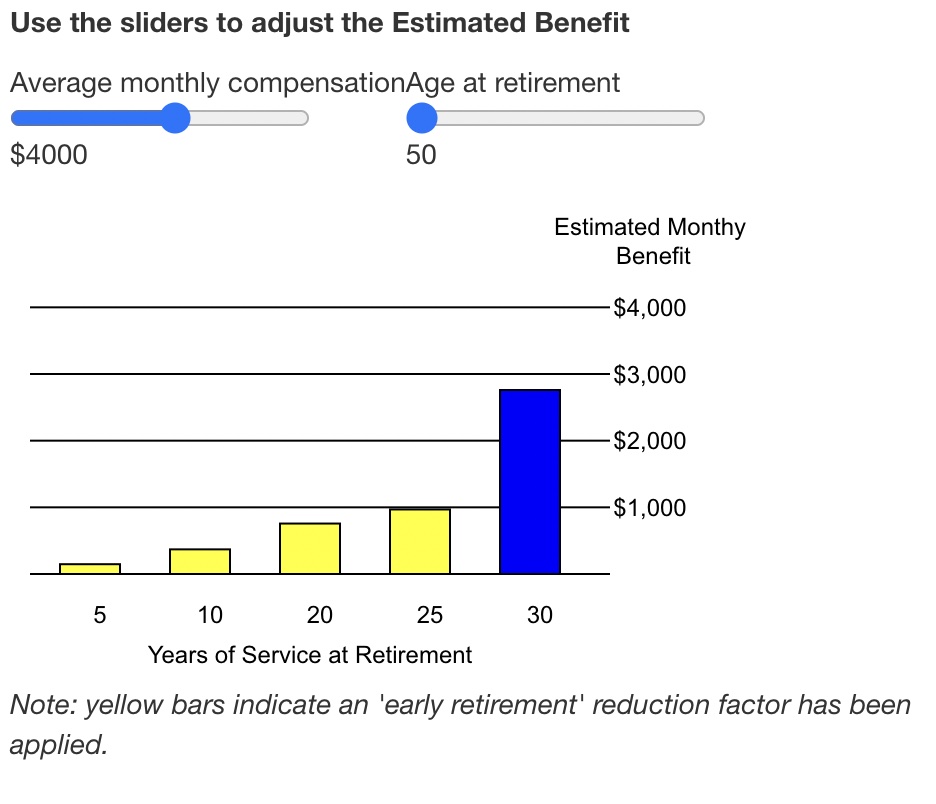

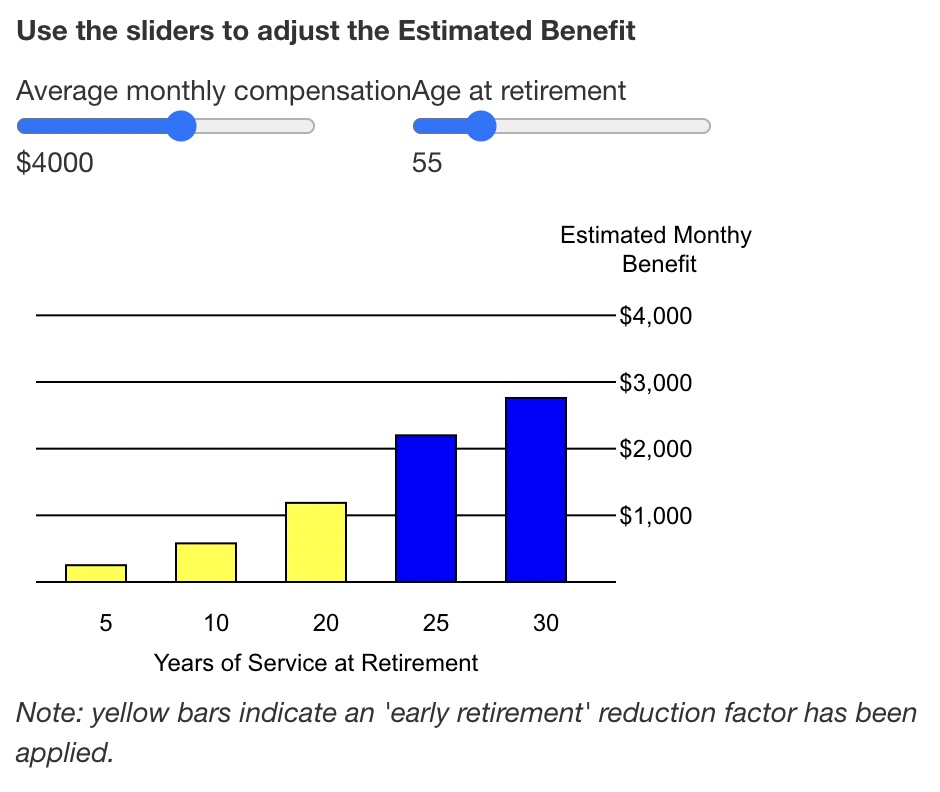

You can retire as early as age 50 with five years of service, but you need to understand there are actually two different ways your benefit gets reduced. First, the fewer years you work, the lower percentage of your income gets replaced in retirement. As you can see in the wage replacement table, someone with 15 years gets 31.5% of their salary replaced, someone with 25 years gets 55% replaced, and someone with 30 years gets 69% replaced. That’s a massive difference in your standard of living in retirement – nearly doubling your pension by working those extra 15 years.

Second, if you retire before your normal retirement age, there’s an additional early retirement penalty on top of that. This penalty is 5% per year from age 50 to 60, and 3% per year from age 60 to your normal retirement age. So you’re getting hit twice – once for having fewer working years, and again for retiring early.

Here’s what this looks like in practice: Let’s use the ASRS benefit calculator as an example. Someone with a $4,000 average monthly salary who retires at age 55 with 25 years of service gets about $2,100 per month – that’s the blue bar in the first image. But look what happens if that same person retires at age 50 with 25 years of service (second image). Now they’re only getting about $1,000 per month instead of $2,100. That’s less than half! You can see how the yellow bars (early retirement) are much lower than the blue bars (normal retirement) even with the same years of service. This is the early retirement penalty in action. Over a 30-year retirement, that’s the difference between receiving $756,000 versus $360,000 in total pension payments – a $396,000 difference for retiring just 5 years early.

Now money is not the end all, be all. So in some cases it’s perfectly fine for you to make a decision that will lower your monthly income in retirement, if it means you get to retire earlier and you still have enough to live on. There’s a balance there and I’m not a financial planner who is always going to defer to the answer that makes you the most money. But I don’t want you to go into this decision blind, or ignorant about the long term effects of your decision.

Working until your normal retirement age gives you the maximum benefit calculation, but you need to weigh that against the value of having extra years in retirement.

The key factors to consider: your health, other income sources, what you want to do in retirement, and how you’ll bridge the gap until Social Security kicks in.

Decision #3: Working After Retirement

Many retirees want to work part-time or return to work, but there are rules you need to understand.

You can work for non-ASRS employers immediately with no restrictions. So if you have enough years of service in your 50s or early 60s and you still feel like working, you can do that with no impact to your pension.

But if you want to work for an ASRS employer – like going back to your same employer, or even trying something new with the Arizona State System, there are waiting periods, hour limitations, and earnings restrictions. The key rule to understand is the “20/20 criteria” – if you work 20 or more hours per week for 20 or more weeks in a fiscal year, your pension will be suspended and you’ll become an active member again. Violating these rules can affect your pension payments, so you need to understand them before you retire.

The best strategy here is planning your post-retirement work before you retire from ASRS. Whether that’s positioning yourself for consulting opportunities in the private sector, understanding the waiting periods for returning to ASRS employers, or planning how to stay under the hour limits – these decisions should be part of your retirement planning, not something you figure out after the fact and certainly not something you accidentally violate.

Decision #4: Healthcare in Retirement

Health is a significant expense in retirement, and ASRS has benefits that most people don’t even know about.

The Health Insurance Premium Benefit provides $50 to $260 per month toward your health insurance premiums (depending on your years of service) if you have five or more years of service and keep ASRS-eligible health coverage.

With 30 years of service, that’s $260 monthly, or $3,120 per year. Over 15 years of retirement, that’s nearly $47,000 in benefits. This benefit only applies to ASRS-sponsored plans or non-subsidized employer coverage – you lose it if you go with private or marketplace insurance. You can still receive this benefit when you become Medicare-eligible, but you must enroll in an ASRS Medicare plans and the benefit amount is reduced.

Now here’s the decision most people don’t know they have to make: the Optional Premium Benefit. This is a one-time election at retirement where you can take a reduced premium benefit that continues to your spouse after you die. Let’s say instead of getting the full $260 monthly benefit that dies with you, you elect to receive $200 monthly, but your spouse continues to get that $200 monthly after you pass away.

You can only make this election if you choose a Joint and Survivor pension option, and your spouse must be eligible for ASRS health coverage. But over two lifetimes, this optional benefit could be worth $50,000 or more compared to the standard benefit.

When you’re leaving ASRS employment and looking for new health insurance, a marketplace plan might look cheaper at first glance, but when you add in the ASRS premium benefits, the ASRS coverage might actually be the better deal. You really just need to run the numbers as well as the coverage to see what’s best for you.

How These Decisions Work Together

These four decisions don’t exist in isolation. They all affect each other, and all have a place in your financial plan.

Your age and years of service at retirement affects your monthly pension, which affects your survivor benefit amounts and could influence your decision there. Health care will be an ongoing and potentially increasing expense of your life, and you don’t want to put yourself in a position where you can’t afford the care you need.

Your survivor benefit election affects whether you can choose the Optional Premium Benefit. And your return to work after ASRS employment could be crucial to allow your portfolio to grow a little bit longer before you start taking distributions.

These aren’t decisions you want to figure out as you’re walking out the door on your last day. Take the time now to understand your options, run the numbers, and create a plan that works for your specific situation.