If you’re a teacher, state worker, or public employee in Arizona, you probably feel pretty good about your pension. And you should, most people don’t have pensions which is a very valuable source of lifetime income. But, it’s not perfect. In particular, there are three major problems that everyone needs to fully understand as they prepare for their retirement.

This post is meant to help you actually do something about some of these issues while you still have time.

Problem #1: Zero Inflation Protection

Let’s start with the first problem, and it’s a big one. Your ASRS pension has zero inflation protection. Zero.

What does that mean? It means if you retire with a $3,000 monthly pension, you’ll get $3,000 every month for the rest of your life. Which sounds good to start, right? Well, here’s the problem: $3,000 today won’t buy you $3,000 worth of stuff in 10, 20, or 30 years.

Assuming 3% inflation rate, which is right around the historical average, here’s what happens to your purchasing power:

Year 10: Your $3,000 only buys about $2,230 worth of stuff

Year 20: Your $3,000 only buys about $1,660 worth of stuff

Year 30: Your $3,000 only buys about $1,236 worth of stuff

You’re essentially taking a pay cut every single year of retirement.

Imagine if your salary never went up for 20 years while everything else got more expensive. That’s essentially what happens with your ASRS pension.

The good news? You can plan for this. That’s where your 403(b), 457 plan, and other savings come in. They can potentially grow over time to offset this challenge.

Problem #2: The Income Replacement Gap

This brings us to problem number two: the income replacement gap.

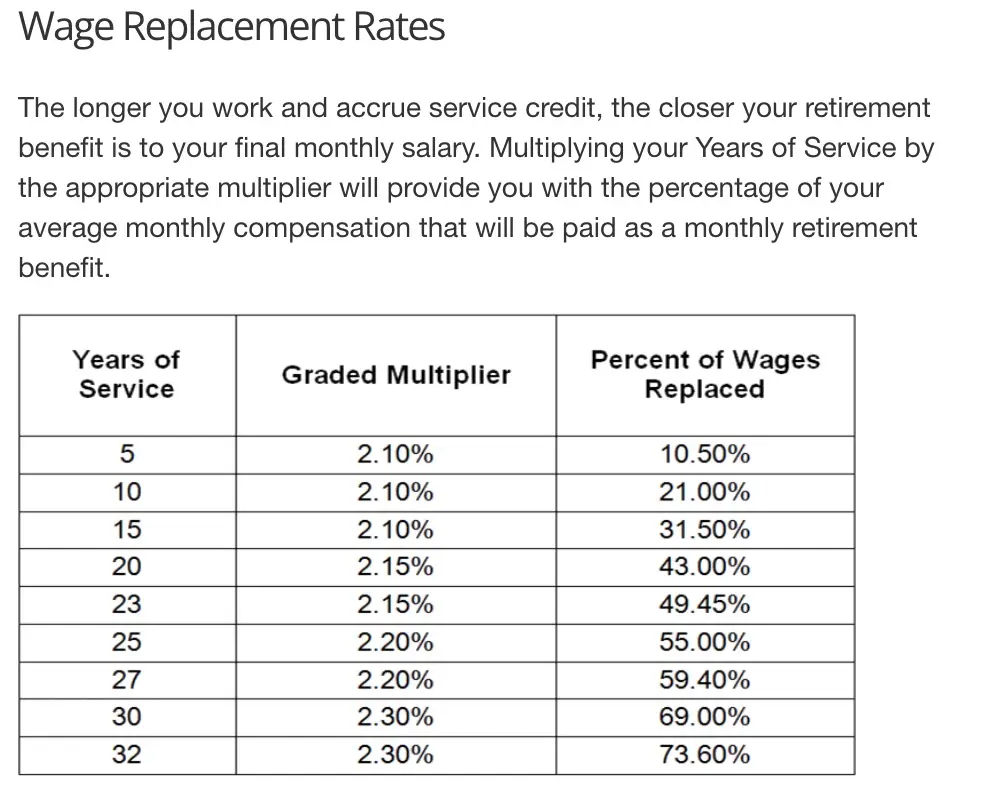

Financial experts generally recommend that you replace 80 to 90% of your pre-retirement income to maintain your standard of living. I don’t necessarily love that rule of thumb but it still brings up an important point: Your ASRS pension, if you work there for 30 plus years, is only going to cover around 70% of your pre-retirement income.

And if you’re like most people, it’s going to be much less. Someone who has worked for there 20 years, which is quite a long time to stay at one place, will only have 43% of their income replaced.

Here’s what this means in real dollars: Let’s say you’re making $60,000 a year when you retire. If you have 20 years of service, your ASRS pension will give you about $2,150 per month – that’s $25,800 per year. You’re going from $60,000 to $25,800. That’s a massive lifestyle change.

Even if you’re one of the lucky ones who stays for 30 years, you’re still looking at a significant drop. That same $60,000 salary would generate about $3,450 per month, or $41,400 per year. Better, but still a $18,600 annual pay cut.

And remember, we haven’t even talked about taxes yet. Your pension is fully taxable as ordinary income, so that gap gets even wider after Uncle Sam takes his share.

The reality is that your ASRS pension is a great foundation, but it’s not designed to be your entire retirement plan. It’s designed to work alongside your other retirement savings. The sooner you understand that gap, the more time you have to fill it through additional savings and smart planning.

Problem #3: The Tax Trap

Now we get to problem number three, and this is the one that really catches people off guard: the tax trap.

ASRS members really need to know that your entire pension is taxable as ordinary income. Every dollar. There’s no special tax treatment, no breaks, it’s all taxed at your regular income tax rates.

But it gets worse. You’re facing a triple tax hit:

•100% of your ASRS pension is taxable

•Up to 85% of your Social Security is taxable

•All your traditional 403(b) and Traditional IRA withdrawals are taxable

With all of those income sources taxed at ordinary income rates, you might be paying a similar tax rate in retirement as you were in your earning years.

And here’s the scary part: tax rates might be even higher in 10 to 20 years. With the national debt where it is, with our annual deficits that have occurred basically every year this century, and our politicians kicking the can down the road on making tough fiscal changes, a lot of people think that tax rates will have to go up eventually. So you could be paying higher taxes on an income that’s losing purchasing power every year.

What This All Means for You

The ASRS pension is not perfect. The math is pretty clear. Between inflation eating away at your purchasing power year after year, the significant income replacement gap, and taxes taking their bite out of multiple income sources, your pension alone isn’t going to provide the retirement lifestyle you’re probably expecting.

But it’s still a very valuable benefit that most Americans would love to have. Your ASRS pension is a great foundation, but you need to build the rest of your retirement plan around it.

The good news? Now that you know about these three hidden problems, you can actually do something about them. Don’t be one of those people who waits far too long to make any real changes to their retirement strategy.

Next week, I’ll be sharing my step-by-step action plan for ASRS members, including how to use your 403(b) and 457 plans to fight inflation, smart strategies for filling that income gap, and tax moves that can save you thousands in retirement.