The numbers are sobering: nursing home care now costs over $108,000 annually, home health aides run $60,000-80,000 per year, and the average person needs care for about 2.5 years. With only 7.5 million Americans carrying long-term care insurance, most of us will be paying these bills ourselves.

But here’s what most financial advice gets wrong: the “best” account for long-term care isn’t always the one with the biggest tax advantages. The smart strategy depends on when you need care and how much you’re spending. Use the wrong account at the wrong time, and you could waste thousands in tax benefits.

Why Account Choice Matters

Every retirement account has different tax rules, and long-term care sits at the intersection of several important tax considerations:

The medical expense deduction threshold: Healthcare costs exceeding 7.5% of your adjusted gross income are deductible. If your AGI is $60,000, you only need $4,500 in medical expenses to start claiming deductions. With long-term care bills, you’ll blow past this threshold quickly.

Required minimum distributions: After age 73, you must withdraw from traditional retirement accounts anyway. This timing often aligns perfectly with when people need long-term care.

Tax arbitrage opportunity: When you have large medical deductions available, it actually makes sense to generate taxable income that gets offset by those deductions. This flips conventional wisdom on its head.

The Ideal Withdrawal Order for Long-Term Care

1. Traditional IRA/401(k)

This might surprise you, but traditional retirement accounts are often your best bet for major long-term care expenses.

Here’s why: withdrawals from traditional accounts create taxable income, but when you’re paying $80,000+ annually for care, you’ll easily exceed the medical expense deduction threshold. The deduction can potentially offset a substantial portion of the taxes on your withdrawal.

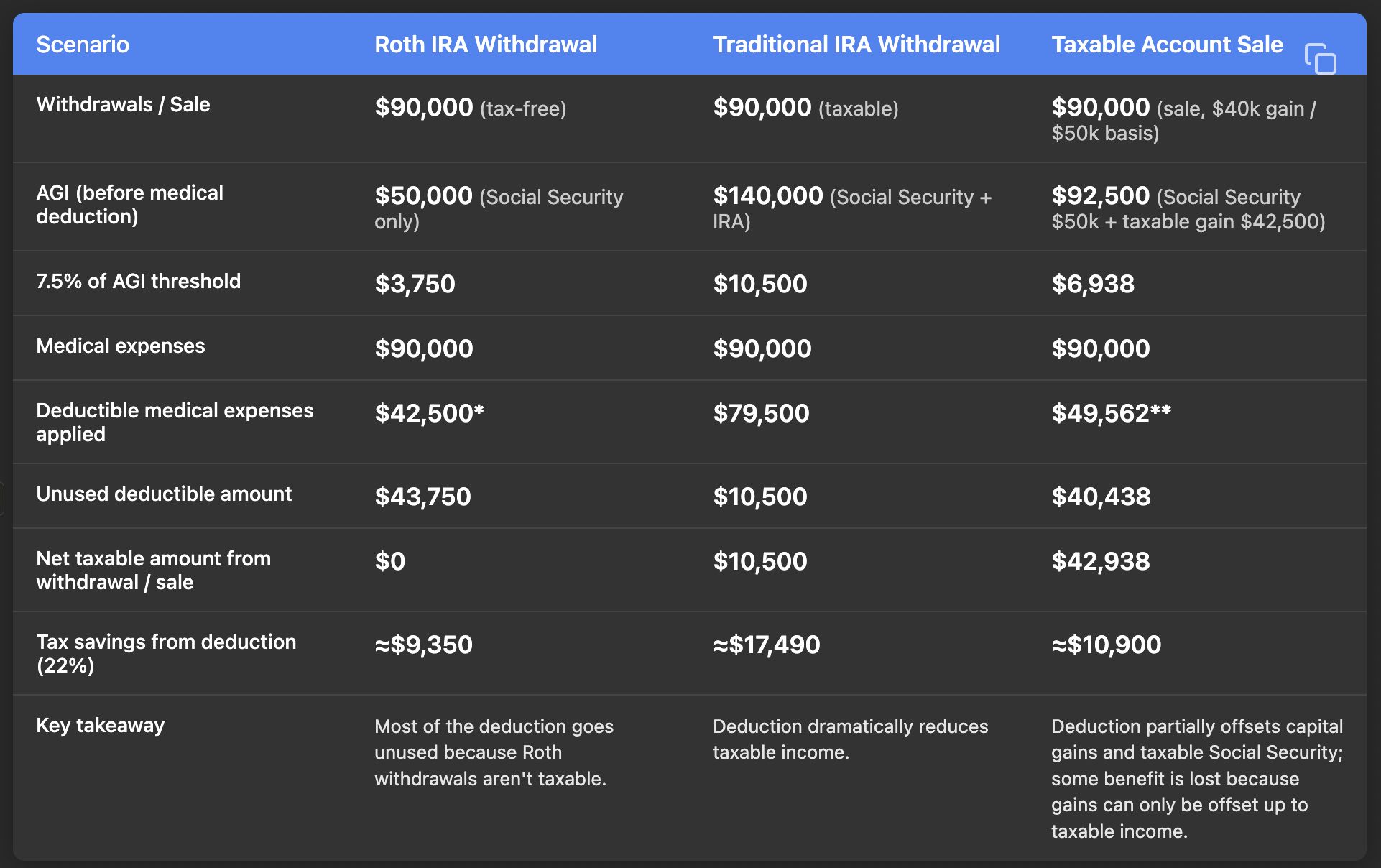

Consider this example: You have $50,000 in Social Security income and withdraw $90,000 from your traditional IRA to pay for nursing home care. Your total AGI is now $140,000. Medical expenses above $10,500 (7.5% of AGI) are deductible—meaning $79,500 of your $90,000 in care costs can potentially offset a substantial portion of the taxes on your IRA withdrawal.

Plus, you’re required to take distributions from these accounts after age 73 anyway. Using them for long-term care essentially makes those forced withdrawals tax-neutral. And if you don’t use these funds during your lifetime, your heirs will face the full tax burden on inherited traditional IRA assets—making it even smarter to spend them on deductible medical expenses while you can benefit from the tax offset.

2. Taxable Accounts

Taxable investment accounts offer excellent flexibility for long-term care funding. While you’ll pay capital gains tax when you sell appreciated securities, you can still claim the full medical expense deduction for your care costs, which can offset some of the tax bill from both the capital gains and other income.

These accounts also have no age restrictions or required distributions, giving you complete control over timing. And if you don’t end up needing all the funds for care, taxable accounts benefit from a step-up in cost basis for your heirs.

3. Roth IRA

Roth IRAs provide tax-free withdrawals, which sounds ideal until you consider the medical expense deduction angle. Since Roth withdrawals don’t create taxable income, you can’t benefit from medical expense deductions that could offset taxes.

To illustrate the difference, let’s compare this to the Traditional IRA example above. Suppose you have the same $50,000 in Social Security income and withdraw $90,000 from your Roth IRA to pay for nursing home care. Your AGI stays at $50,000 because Roth withdrawals aren’t taxable. That means only expenses above $3,750 (7.5% of $50,000) are deductible, so you’d have about $86,250 of deductible medical expenses. But here’s the problem: without any taxable income from those Roth withdrawals, those extra deductions go unused. In this example, roughly $36,000 of potential deductions would be wasted simply because there’s no taxable income to offset.

Roth distributions work well when your long-term care expenses are relatively light—say, a few hours of home health aide services per week that don’t push you over the 7.5% AGI threshold. Or if you’ve already depleted your pre-tax accounts as well as your taxable accounts.

But we have to remember that Roth IRAs are also the most valuable accounts to leave to heirs, making them worth preserving if possible (and if leaving money to your beneficiaries is a priority to you).

Here’s a comparison of these three choices, using the example above:

4. Health Savings Account

HSAs offer a triple tax benefit: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Long-term care definitely qualifies.

But here’s the counterintuitive problem: HSAs are almost “too good” for heavy long-term care years. When you use HSA funds for medical expenses, you can’t also deduct those expenses on your tax return. During years when you’re paying massive care bills that would generate valuable deductions anyway, using your HSA means forgoing those deductions.

HSAs work best for lighter long-term care expenses or other medical costs throughout retirement. Just remember: contribution limits ($4,300 for individuals, $8,550 for families in 2025) make it difficult to build a substantial long-term care war chest, especially if you start late.

Putting It Into Practice

Early Retirement/Before Care Needs: Keep your HSA invested and growing. Use other accounts for living expenses while preserving the HSA’s tax advantages for future medical needs.

Light Long-Term Care Years: When you need some assistance but costs are manageable, tap your Roth IRA or HSA. These tax-free withdrawals won’t generate much in medical deductions anyway, so you might as well use the accounts with the best tax treatment. HSAs are also useful in high-tax retirement years. For example, if you’re doing Roth conversions and have pushed your income up, HSA withdrawals for medical expenses won’t add to your tax burden.

Heavy Long-Term Care Years: This is when you prioritize traditional IRAs and 401(k)s. The medical expense deductions will largely offset the taxes, making these withdrawals essentially tax-neutral. Taxable accounts work well here too.

Legacy Planning: Preserve Roth accounts and taxable accounts (which get a step-up in basis) for your heirs when possible.

Why Tax Diversification Is Essential

The withdrawal strategy above only works if you have money spread across different account types. Without tax diversification (savings in traditional, Roth, HSA, and taxable accounts) you can’t optimize based on your actual care needs.

Start building now: Don’t put everything in your 401(k). Fund Roth IRAs, HSAs (if eligible), and taxable accounts to create options for later.

Inheritance considerations: HSAs lose tax benefits for non-spouse heirs, and traditional IRAs will be taxed by heirs, adding more reasons to use these accounts strategically and while you are still with us.

The Bottom Line

There’s no single “best” account for long-term care. The key is building tax diversification early and then thinking in terms of withdrawal sequencing and tax trade-offs rather than simply maximizing tax-advantaged contributions.

The right withdrawal order can help your assets last longer and reduce the total tax drag on your long-term care spending. In a world where care costs continue climbing, every tax dollar saved is a dollar that can fund more care or pass to your heirs.