For many Americans, Social Security is an extremely valuable tool in generating the retirement income that they need to be comfortable. Because of its importance, I strongly recommend exploring all of your options before you make a decision on when to claim it.

The most common age that people take their Social Security benefits is age 62, right when they are first eligible.

Now this may be because they simply need the income, and I certainly understand that.

However, there are also a number of people who simply don’t understand all the implications of taking Social Security that early.

So the point of this episode is to help you understand all that’s considered when you start taking your Social Security benefits, so you can make an informed decision.

Here Are Some Questions To Consider Before Claiming Social Security:

- When do you want to receive your retirement benefits?

- Should you wait until you can receive a higher benefit amount?

- Do you want to work past Full Retirement Age?

- Do you want to retire early?

- If you want to retire early, will you need Social Security to get by, or can you use other sources of income and assets while you delay Social Security?

- Do you have any known health issues that might affect how long you live?

1. Receive Benefits Early (Before Full Retirement Age)

You can make the decision to receive your benefits early if you wish to, before your full retirement age. The earliest you can claim your benefit is at age 62 (there are some exceptions to this, in the case of a widower, which we’ll discuss later).

Remember though: The amount of benefits you receive will be reduced. If you take your Social Security at age 62, you’ll only be receiving 70% – 75% of your possible benefits, depending on the year you were born.

You need to wait until Full Retirement Age to receive 100% of your benefits.

If you decide you still want to take your benefits early, then the next question for you to consider is whether you will continue working or retire completely. This is a very important decision because it will have an impact on your Social Security benefits.

Stop Working Entirely And Claim Social Security Benefits

If you decide to stop working before your full retirement age and choose to receive benefits, the Social Security office actually REDUCES your benefits.

Per the Social Security website: “A benefit is reduced 5/9 of one percent for each month before normal retirement age, up to 36 months. If the number of months exceeds 36, then the benefit is further reduced 5/12 of one percent per month.”

If that isn’t clear, let me try to rephrase: Social Security will reduce your benefit by a small fraction of a percent for every month that you take it early. And the reduction is on a sliding scale.

Meaning, if you take your benefits at age 63, then the amount you receive will be higher than it was at age 62. The longer you delay receiving your benefits, the more the benefit amount will grow. And that is true all the way up until age 70.

So that’s one option you have: Stop working entirely and take your social security benefit before your full retirement age, at a reduced amount.

The Other Option Is To Take Your Social Security Benefits Early And Continue Working

Choosing to continue to work and receive benefits will put you in the same boat as if you stopped working before your full retirement age. You will receive reduced benefits, at the same rate as if you stopped working.

However, there is one big difference: Your benefits will again be reduced if you exceed the yearly earnings limits.

Here’s how it works:

- If you earn too much income while drawing your benefits before your Full Retirement Age, then Social Security will deduct $1 from your benefits for each $2 you earn above $18,240. These numbers are as of 2020.

- If you earn more than $48,600 in the year you reach your Full Retirement Age but before the month you actually attain Full Retirement Age, then Social Security will deduct $1 from your benefits for each $3 above that amount.

- Note: If you earn too much and have benefits withheld, Social Security will readjust your benefit amount to give you credit for any reductions or withholdings they made due to your excess earnings. And they would do this once you reach your Full Retirement Age. In other words, they will pay you back….eventually.

So if you do need the extra income that Social Security would provide (in addition to your working income), just know that your benefits could be reduced, thus lowering the amount of income you hope to receive.

Now that we have an idea of what it would look like to claim Social Security before Full Retirement Age, let’s discuss your second option, waiting until Full Retirement Age.

2. Receive Benefits At Full Retirement Age

Your next option is to wait to receive your benefits at your Full Retirement age, which will be between 66 and 67 years old, depending on when you were born.

If you were born after 1960, then it will be age 67, and if you were born before then, it will be at some point in the year you turn 66. You can find out exactly when it is for you here: https://www.ssa.gov/benefits/retirement/planner/agereduction.html

If you choose to wait until your Full Retirement Age to receive benefits, then you will receive 100% of your Social Security benefit amount. In other words, it won’t be reduced at all, unlike if you were to take it early as discussed previously.

In addition to that, once you reach Full Retirement Age, there is no limit on the amount of earnings that you can have. Per Social Security: “If you work, and are full retirement age or older, you may keep all of your benefits, no matter how much you earn.”

Those two benefits, in my mind, make waiting until your Full Retirement Age something that you should strongly consider. However, there is one more option available to you, that also has some great benefits.

3. Receive Benefits After Full Retirement Age (Up To Age 70)

For every month that you delay taking your social security benefits, they will grow by 8% per year. So from age 62 up until age 70, your benefits can continue to grow (they stop growing at age 70).

I mentioned earlier how at your Full Retirement Age, you will receive 100% of your benefits. Yet if you delay taking your Social Security benefits until age 70, you will earn “delayed retirement” credits, and you will receive around 132% of your possible benefits.

Another added benefit of waiting beyond your Full Retirement Age is that you can potentially increase your benefit amount by replacing the lower earning income years you might have on your record.

There are two ways that working until 70 can increase the amount of benefits you receive:

As previously discussed, Social Security calculates your highest 35 earning years. But if you are still working in your 60s, there’s a good chance that you’re making more (perhaps a lot more) than you were in your 30’s or 40’s. So these more recent earning years could then replace other lower earning years in the calculation of the 35 years of earnings. And that, in turn, will increase your benefit calculation.

Now it is impossible for me to give you a recommendation on when to receive your benefits in this format. There are a number of factors to consider when deciding when to take Social Security, including:

- Your health

- Your cash needs

- Your life expectancy

- Your spouse (and their expected benefits)

- Whether you are still working

All that said, there are some significant advantages to delaying your Social Security Benefits, that I want you to at least consider before making a decision.

What are my expected benefits?

If you don’t already know what you’ll receive from Social Security, I’d encourage you to find out immediately (yes, even if you must put down this book!)

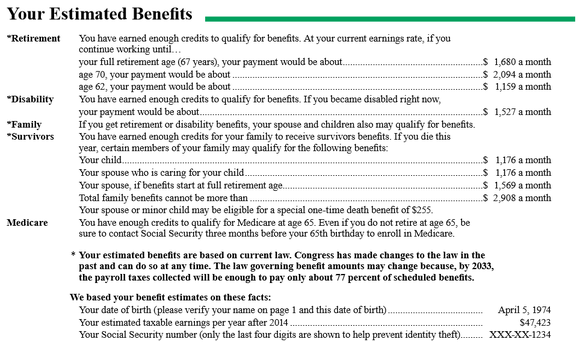

Social Security has a site where you can access your expected benefits: https://www.ssa.gov/myaccount/. You will need to create an account, and verify your identity, and then you’ll receive a Social Security Benefits Statement that looks like this:

After viewing yours, you can get an idea of what income you could expect if you take your benefits early (at 62), at your Full Retirement Age (between 66-67), and at age 70.

You can also see what your Earnings Record, which shows the various income amounts you’ve earned over your earning history. We’ll discuss this in more detail later:

Key Takeaways For Your Social Security Options:

- In Most Cases, You Can Start To Receive Your Social Security Benefits Between Age 62 And Age 70.

- Your Full Retirement Age (Between 66 Years Old And 67 Years Old) Is When You Will Receive 100% Of Your Social Security Benefits.

- If You Claim Your Benefits Before Your Full Retirement Age, Your Benefits Will Be Reduced.

- If You Delay Claiming Your Benefits Beyond Your Full Retirement Age, Your Benefits Will Be Increased (Up To Age 70, After Which They Won’t Grow Any More).

- Social Security Calculates Your 35 Highest Earning Years In Determining Your Benefits.

- If You Take Your Benefits Before Your Full Retirement Age, And Continue Working, Your Benefits Could Be Reduced If You Make Too Much Income

- Review Your Expected Benefits So That You Know Your Options, Even If You Are Years Away From Claiming Your Benefits.