Today we are going to be sharing something really sad and frankly troubling for your finances.

We’re going to be talking about why people have poor returns on their investments. And no, it’s not because the market is doing poorly.

Instead, it’s because of investor behavior, or in other terms, human error. Human behaviors that cause investors to walk away with much lower returns than they could.

Why?

It comes down to behavior mistakes. Not low IQ! Call it fear, greed, or making your investments more complicated than they need to be, not thinking about the long term plan, or a number of other explanations. No matter how you look at it, investor behavior, how people actually act, causes much lower returns than what is possible.

Author Carl Richards wrote about it best in his book ‘The Behavior Gap’ (which I highly recommend you pick up). In it, he says “Studies find that the returns investors have earned over time are much lower than the returns of the average investment.”

One of the most famous studies that do this is by Dalbar, in a report titled Quantitative Analysis of Investor Behavior. Every year, they review the returns individual investors actually get vs what the investment funds actually get. Let’s discuss some of their results.

In a study published in 2020, looking at results through the end of 2019, they looked at the 20 and 30 year returns of individual investors, and they are quite disspiriting.

Over a 20 year period, individual investors invested in equities (stocks) got a 4.25%. In that same time period, the S and P 500 (the most famous index that tracks the largest 500 companies in the US) got a 6.06% return. That means that individual investors got a 1.81% lower return than an index that they easily could have bought, held onto, and just reinvested in quite simply.

Over a 30 year period, though, the results were even worse. The average investor invested in equities got a 5.04% while the S and P 500 returned 9.96%. That is a difference of 4.92%.

That phenomenon is the behavior gap, and it’s a serious problem when you think about the decades of compounded earnings you could be getting, but you don’t, because you have these behavioral mistakes.

In terms of real dollars, those lower returns really add up.

Let’s do some simple math. Let’s say you start out with $100,000, contribute $10,000 annually, and for 20 years you get the average investor return of 4.25%. Over 20 years, you’ll end up with $548,504.71. Not bad.

But if you remove those behavior mistakes, and just get the S and P 500 returns of 6.06%, using all the same assumptions you would have ended up $717,037.63. That’s a difference of $168,532.92. So if the average investor removed those behavior mistakes, that behavior gap, they would have $168K more to spend in retirement.

If we do that over 30 years, the difference is even greater. Again, let’s say you start out with $100,000, contribute $10,000 annually, and for 30 years you get the average investor return of 5.04%. Over 30 years, you’ll have $1,139,847.28. Again, that’s a decent chunk of change!

However, if you can remove those behavior mistakes, and just get the 9.96% that the S and P 500 got, you would have ended up with $3,521,139.68.

So we know there is an issue in terms of people getting in their own way, and for the rest of today’s episode I want to talk about, why is that? Why don’t people at least get returns equal to the investments that they own?

Dalbar has some insights on this in general, and then I will discuss 5 reasons why investors fall prey to these behavioral mistakes.

Here’s what Dalbar has to say about it: “Investor behavior is not simply buying and selling at the wrong time, it is the psychological traps, triggers and misconceptions that cause investors to act irrationally. That irrationality leads to buying and selling at the wrong time, which leads to underperformance.”

That’s a good summary, and now let’s discuss 5 of those reasons in more detail.

1. Letting Your Emotions Get In The Way

There are a number of emotional landmines that get in the way of good investing.

One big emotional mistake is that you don’t stay invested in the market because you think prices are “too high”, and you decide to wait until things “cool off.” I’ve heard this from a number of people, and it’s honestly not a good idea. I’ve also done a podcast on that topic, titled Should You Invest In Stock Market Highs? It’s episode #40 of Retirement Clarity Radio

The fact is, the stock market is continually hitting new highs, and the highs that we have today, if history holds true, which we know isn’t a guarantee, but the highs we have today will be lows in 5, 10 and 20 years from now.

Another big emotion mistake is when something causes a drop in the market, like the Coronavirus, or the Great Recession, you decide to sell everything. We all know we shouldn’t, but it’s still tough emotionally to hold onto our investments when they are seemingly falling every day during big events like that.

Or maybe you see a hot new investment (like Bitcoin, the Reddit stocks, or Tesla) and you jump into those investments after they have already experienced incredible gains. Leaving you holding a very overvalued investments at the tail end of its ride upward.

There are all potential ways that your emotions could end up causing this behavior gap.

As with all things in personal finances, knowing your own emotional tendencies will help you create the right financial plan and investment strategy which will help you avoid these common and costly pitfalls.

2. Thinking You Are Too Good/Too Smart to Buy and Hold

As you can imagine, as a financial planner, I speak to a lot of people about their money and investing. One very familiar refrain that I hear is “why would I buy and hold? Why not buy low, sell high?”

I’ve spoken about this before, but I’ll say it again: I don’t know of anyone who has successfully been able to predict market trends, to determine what is the “high” point for the market, so they know when to sell. And I don’t know anyone who has consistently been able to buy back in when the market is at a “low”?

If those people exist, please let me know!

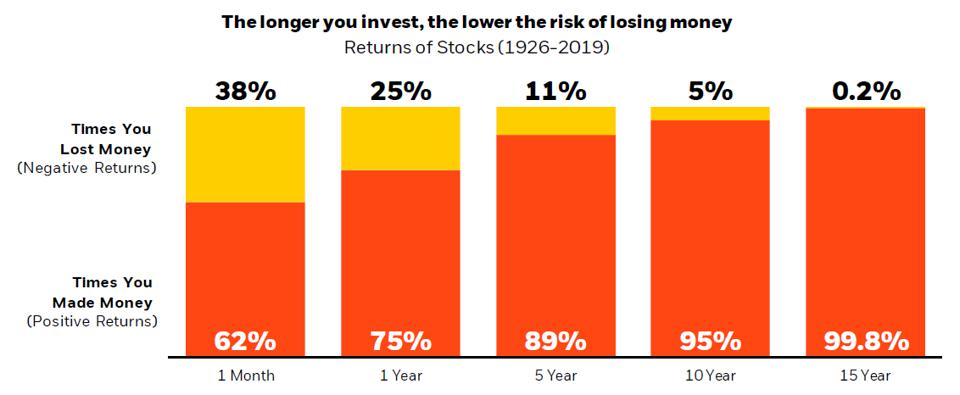

But the top investors of all time are the ones who do not engage in this behavior, and don’t try to pretend they know what the market will do in the next week, month, or year.

In addition, over the next 10 and 20 years, though, we can be very confident (though not a guarantee) that the market will rise.

Source: Blackrock

Now is there more to investing than just buying once, and never looking at it again until you retire? Yes, of course there is. Things like rebalancing, tax loss or tax gain harvesting, reviewing for newer/better funds, distributing from the right funds at the right time, and more are all things that you need to do.

So maybe the proper way to describe it is to buy, monitor, tweak, and hold.

Either way, however we describe it, we know what we don’t want to do, which is buying, then selling, then buying back in again, and then selling, and repeating this process continually.

3. Trying To Overcomplicate Your Investment Strategy

Now this main point is relatively clear, and to highlight this point, there are three great quotes from Carl’s book I want to share, and add a little commentary to them.

1. “Over the long term, very few active money managers are able to earn better returns than simple index funds. The best investment strategy is often the simplest investment strategy.”

Even the best money managers in the world cannot consistently beat index funds that buy and hold on to their investments. Not to be rude, but what makes you think that you can outperform them?

When you overcomplicate your investment strategy, you usually see worse performance. It may feel ‘sophisticated’ or like your investments must do better because they are complicated, but historically, they do worse.

2. “You don’t have to choose the perfect investment or save exactly the right amount. You don’t have to predict your rate of return, spend hours watching television shows about the stock market or surfing the Internet for stock picks. You don’t need a plan for every contingency.”

No one can predict the ‘perfect investment.’ The only time you’ll know an investment was right is when it’s in your rearview mirror.

Not only is it impossible, it’s not even necessary! You don’t need to get the returns of Warren Buffett to hit your financial and retirement goals. You can still retire comfortably with the returns that a low cost, well diversified portfolio can generate for you.

3. “Slow and steady capital is short-term boring, but it’s long-term exciting.”

Try to not stalk your portfolios, checking in on them every day or every week. In the short term, there won’t be much of any changes.

Instead, let them do their thing and you’ll see that in the long-run you’ll walk away with much larger gains than if you took the short term exciting route which usually means smaller gains or or even losses.

So please, do NOT abandon a low cost, well diversified portfolio because you think it’s too boring and too simplistic for your needs.

4. Not Looking at Investment Decisions as Life Decisions

Too many of us look at investment decisions as “how do we get the best possible return?”

But look at other life decisions you make. Do you make every other decision in life in terms of the total cost? Of course it’s a factor, but I hope it isn’t the only factor. When you decide what car you want, or house you want, do you always go to the cheapest option because it’ll put the most money in your pocket? Again, I hope not!

I hope you decide how it aligns with your life, your style, your comfort, yes your budget, and you mix all those together and then you decide.

Treat your investments the same way. Look at them as life decisions where the total dollar amount isn’t the only factor.

As Carl Richards says “financial decisions aren’t about getting rich. They’re about getting what you want – getting happy.”

What goals will this money help you achieve in the long run? Will you use the funds to retire or achieve other financial goals?

Again, going back to Carl Richards: Become clear on what you want out of life, then make financial decisions (which includes your investment strategy) that align with what you want.

That’s key to successful investing, as well as a happier and more fulfilling life.

5. Thinking you can do it Yourself

This might be the largest problem. Too many investors think they can do it themselves. They’ve done their research and can make their investment decisions.

But again, when emotions, rash decisions, and inaccurate planning get in the way, you’re left with less than optimal results.

Instead, let a financial planner help you make these decisions. You’ll have a neutral third party who can help you come up with the right financial plan and investment strategies to help you make the right decisions as well as help you avoid the behavior gap to help you achieve your goals.

Now if you think I’m biased, well, of course I am! But you don’t just have to take my word for it. Numerous studies done by independent third parties have said the same thing. Vanguard, Russell Investments, and Morningstar have all studied the issue and shown that the value of working with an advisor can exceed the price that you pay.

One very important value add of a good financial planner is that they will be the barrier between you and behavior mistakes that will derail your financial and retirement goals.

Final Thoughts

If you’re earning less than the market returns, you aren’t alone. The average investor does the same thing. But, there are ways to change it. It comes down to changing your behaviors, and putting guardrails in place so that you don’t make those mistakes yourself.

One way you can do that is by hiring a financial planner to not only help prevent these biases and mistakes, but you also get their expertise, as well as the ability to delegate numerous responsibilities to them.

Fellow financial planner and writer Ben Carlson said it best “The Behavior Gap tells us that financial plans are worthless but the process of financial planning is extremely important. A plan assumes you know what’s going to happen in the future. Which we all know is next to impossible. But consistent planning assumes you admit things will be unpredictable and act accordingly.”

I hope this is helpful, and if you would like to learn more about creating the right retirement plan and investment strategy, you can set up a time for us to speak at StartMyRetirement.US.